research hub

Find What You Need. Learn Something New.

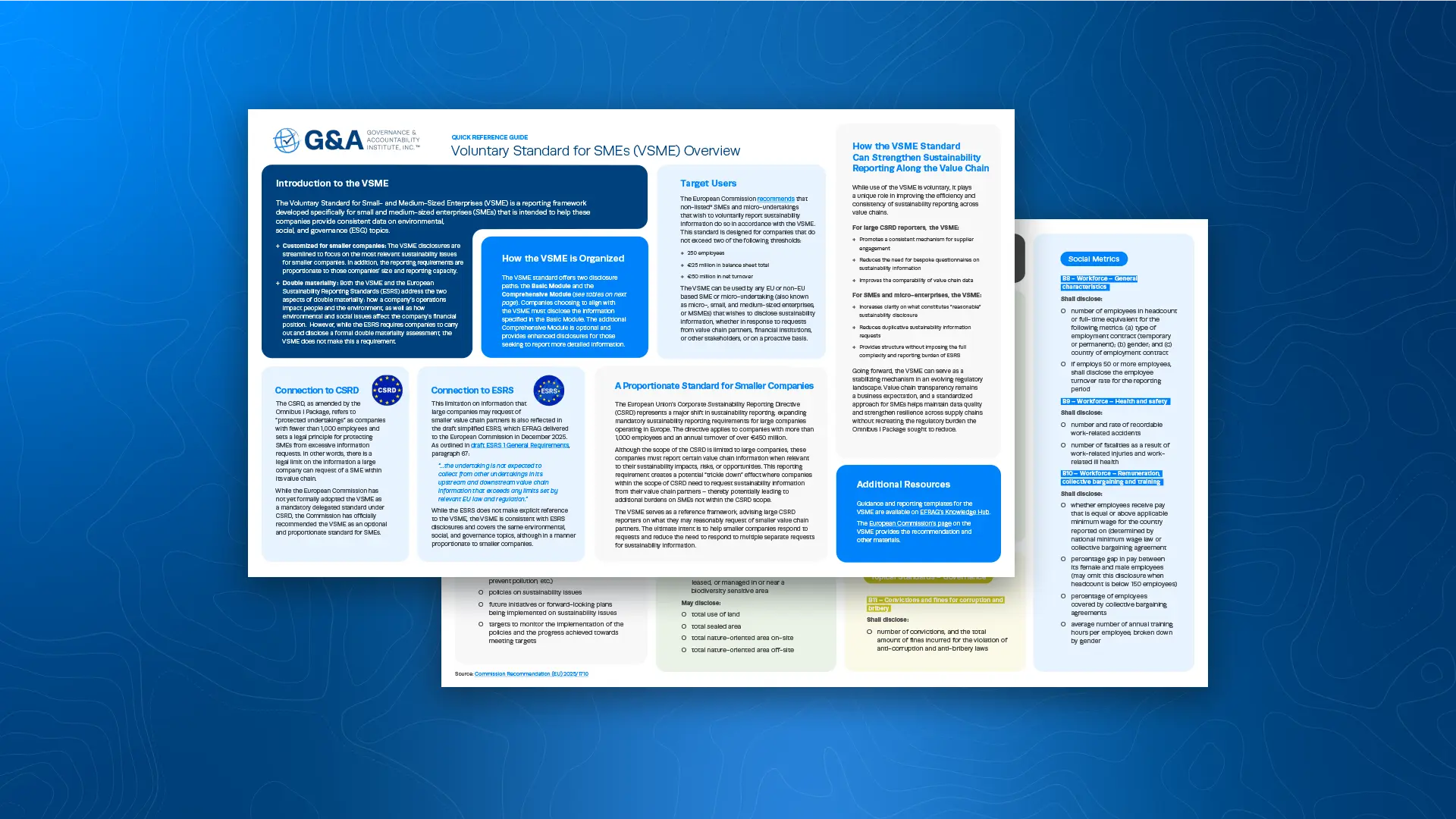

Quick Guide

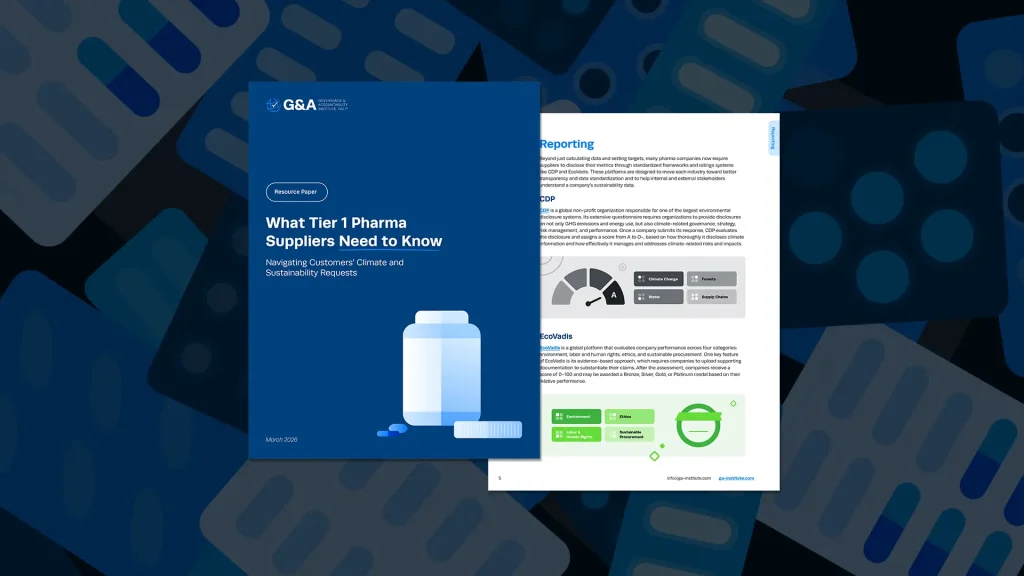

March 25, 2026

March 25, 2026

- All

-

Reporting Trends

-

Resource Paper

-

Quick Guide

-

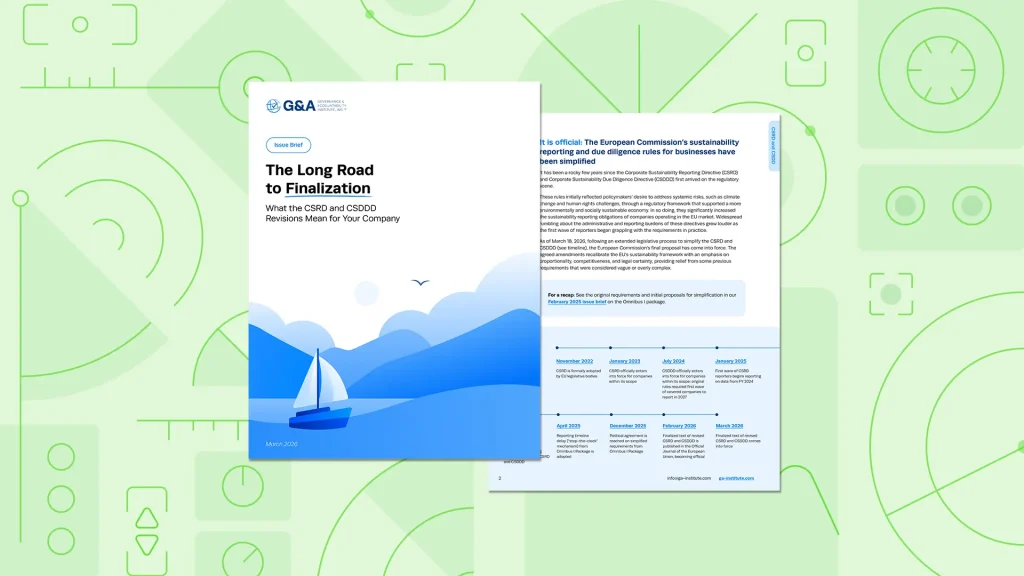

Issue Brief

-

Research Report

-

Collaborations

March 18, 2026

March 4, 2026

February 10, 2026

January 27, 2026

January 15, 2026

November 19, 2025

November 12, 2025

October 28, 2025

October 15, 2025